Search

Published on:

China Year-in-Review: Securing the Battery Supply Chain

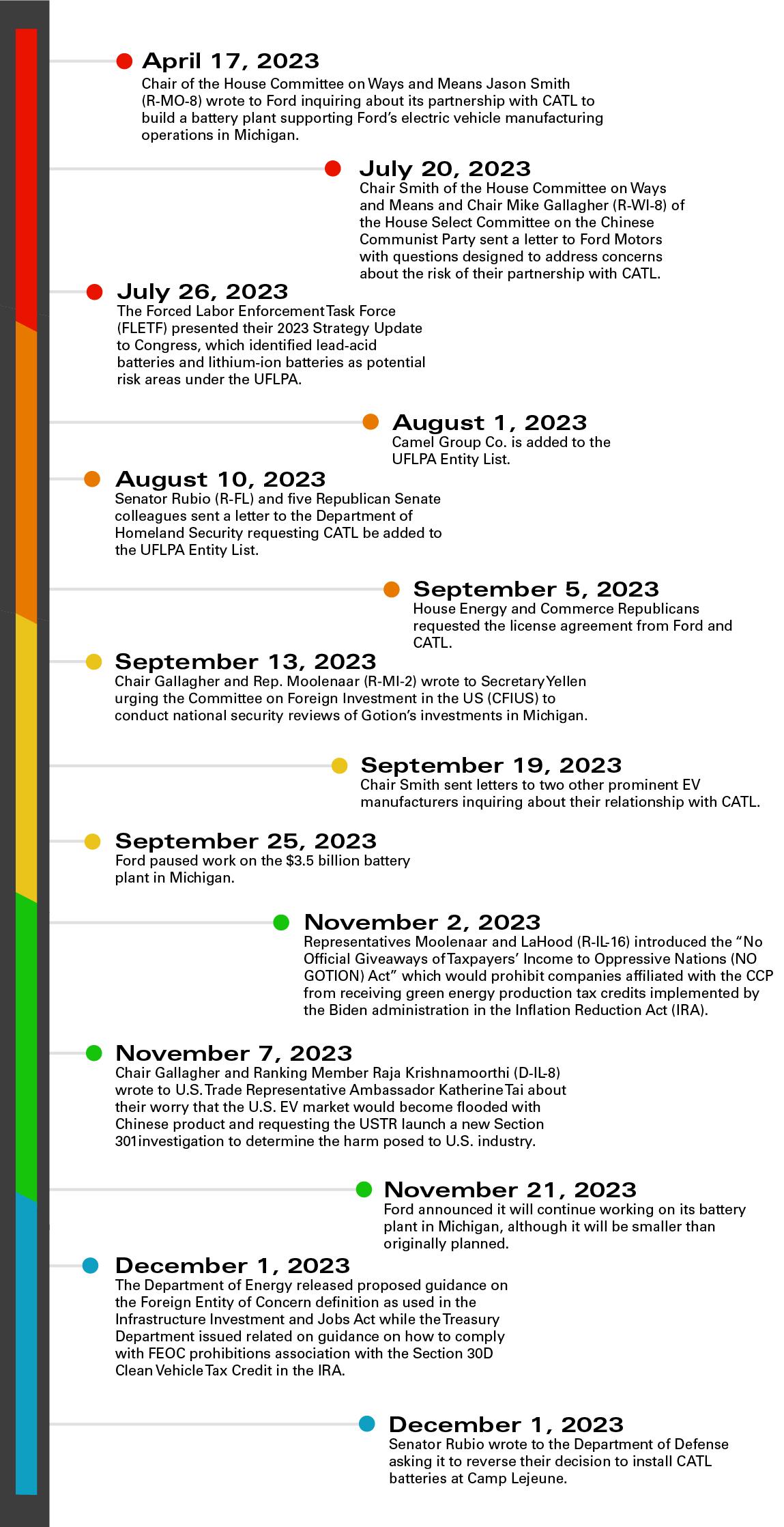

During 2023 both Congress and the Biden Administration repeatedly expressed the need to secure critical supply chains, particularly batteries that rely heavily on lithium and critical minerals sourced from China. Concerns have been framed in terms of national security focusing on the danger of relying too heavily on products integral to our defense or economy or human rights relating to enforcement of the Uyghur Forced Labor Prevention Act (UFLPA).

Congress has conducted investigations, held hearings, and introduced legislation addressing the role of Chinese battery companies in the U.S. supply chain. Contemporary Amperex Technology Co. Limited (CATL) and Gotion High-Tech Co. (Gotion) in particular have drawn Congressional attention in connection with their role as partners to U.S. businesses as well as their ability to benefit from U.S. tax credits under the Inflation Reduction Act (IRA). Executive agencies have also issued guidance addressing whether products may or may not be eligible for federal programs if they are “owned by, controlled by, or subject to the jurisdiction or direction” of the Chinese government.

The following timeline highlights these developments:

Uyghur Forced Labor Prevention Act

Battery components have also faced scrutiny under the Uyghur Forced Labor Prevention Act (UFLPA). The UFLPA imposes a rebuttable presumption that all imports of goods, wares, articles, and merchandise manufactured wholly or in part the Xinjiang Uyghur Autonomous Region (XUAR) or produced by entities listed on the UFLPA Entity List, are produced with forced labor, and are thus prohibited from entry into the United States under Section 307 of the Tariff Act of 1930.

In July 2023, the Department of Homeland Security’s Forced Labor Enforcement Task Force (FLETF) presented their 2023 Strategy Update to Congress, which identified lead-acid batteries, lithium-ion batteries, steel and its downstream products, and copper and its downstream products as potential risk areas.

UFLPA Entity List Additions

Senator Rubio (R-FL), called for CATL’s inclusion on the UFLPA Entity List in August. On December 1, Senator Rubio and colleagues sent a letter to Secretary of Defense Lloyd Austin, urging the Department of Defense to reverse its decision to install CATL batteries at Camp Lejeune. In response to the letter, all CATL batteries were disconnected from the North Carolina Marine Corps base on December 6 despite CATL objections that accusations about security threats are false, and that CATL products in the U.S. do not collect, sell, or share data in any way.

On August 1, 2023, Camel Group Co. Ltd. (Camel) was added to the UFLPA Entity List. Camel is headquartered in China and one of the world’s leading manufacturers of car batteries, particularly lead-acid batteries.

Entities identified on the UFLPA Entity List are subject to a rebuttable presumption that the importation of goods mined, produced, or manufactured by that entity is in violation of 19 U.S.C. §1307 and prohibited from entry to the United States. The FLETF considers additions to the UFLPA Entity List based on the criteria described in the UFLPA. Any FLETF member agency can submit a recommendation to add or remove an entity from the UFLPA Entity List.

House Select Committee on the CCP

The House Select Committee on the Chinese Communist Party (CCP) (Select Committee) has been particularly active in addressing batteries sourced from China due to national security concerns and the risk of incorporating products manufactured with forced labor into the U.S. EV supply chain. On July 20, in conjunction with the House Ways and Means Committee, the Select Committee sent a letter investigating CATL’s partnership with Ford Motor Company following on an earlier letter from the House Ways and Means Committee in April. On September 5, the Republican members of the House Energy and Commerce Committee wrote to Ford, requesting the licensing agreement between the two entities and joined the ongoing investigation into CATL’s U.S. activities and partnerships. The Select Committee’s letter also raised concerns about CATL’s relationship with the XUAR region and forced labor practices.

The House Select Committee on the CCP also held a hearing exploring the governance of Chinese companies in the cobalt mining industry of the Democratic Republic of Congo (DRC) and the presence of child exploitation and forced labor in this sector. Approximately 70% of the world’s cobalt comes from the DRC, while 41% of all batteries containing cobalt are imported from China. Witnesses at the hearing called for sanctions, criminal investigations, and temporary suspension of cobalt-related imports in the U.S. until this practice is stopped. This follows the introduction of a bill last summer by Representative Chris Smith (R-NJ), which would have prohibited the import of cobalt mined in the DRC under Section 307 of the Tariff Act of 1930.

Tax Credits

In 2023, both Congress and the Executive Branch addressed the potential for Chinese companies to benefit from tax credits under the Inflation Reduction Act (IRA) and other federal programs designed to stimulate the U.S. economy and promote domestic manufacturing. In addition to reviewing Ford’s partnership, the House Ways and Means Committee issued letters to two other major EV manufacturers inquiring about their contracts with CATL and the potential risk of federal subsidies from the IRA benefitting Chinese companies rather than American workers. Relatedly, Representatives Moolenaar (R-MI-2) and LaHood (R-IL-16) introduced the “No Official Giveaways of Taxpayers’ Income to Oppressive Nations (NO GOTION) Act” which would prohibit companies affiliated with the CCP from receiving green energy production tax credits implemented by the Biden administration in the IRA.

Under the IRA, certain entities were restricted from eligibility for some of the tax credit programs by virtue of their foreign ownership. Section 30D of the Internal Revenue Code, the Clean Vehicle Tax Credit, for example provides a credit of up to $7,500 per qualifying plugin Electric Vehicle or fuel cell electric vehicle purchased by the taxpayer. The tax credit is made up of two components: a $3,750 credit for a vehicle meeting critical mineral sourcing requirements and $3,750 credit for a vehicle meeting the battery component requirements. Under Section 30D, battery components manufactured or assembled by “foreign entities of concern” (FEOC) and critical minerals extracted, processed or recycled by foreign entities of concern do not meet these standards, making the resulting vehicle ineligible for the credit amounts. However, until recently, it was not clear what degree of foreign ownership or involvement, specifically by Chinese companies, would render the product ineligible under the FEOC definition.

In December 2023, the Department of Energy issued proposed guidance on the term “foreign entity of concern,” supplementing the Department of Treasury’s guidance on compliance with FEOC restrictions under Section 30D. According to DOE, a company will be deemed to be a FEOC if it (a) meets the definition of a foreign entity and is “subject to the jurisdiction of” a covered nation or (b) if it meets the definition of a foreign entity and is “owned by, controlled by or subject to the direction of” the government of a foreign country of concern. To determine whether these definitions are met requires a fact-based analysis of the ownership structure and supply chain of the vehicle and its parts. Comments on DOE’s definition were due January 3, 2024, and comments on the Treasury guidance implementing the FEOC definition were due January 18, 2024. While the rulemaking process is ongoing, the battery component restrictions went into effect on January 1, 2024, and the critical mineral requirements go into effect January 1, 2025.

Other Posts in the China Year-in-Review Series: